Why the Union Pacific–Norfolk Southern Merger Could Remake American Freight

For nearly two centuries, American railroading has chased a single dream: one railroad, one waybill, one seamless journey from the Atlantic to the Pacific. The proposed $85 billion merger of Union Pacific and Norfolk Southern — creating The Union Pacific Transcontinental Railroad — would finally make that dream a reality. If the Surface Transportation Board grants approval, the combined network would stretch more than 50,000 route miles across 43 states and connect roughly 100 North American ports. Supporters argue it would be nothing less than the most consequential upgrade to American freight logistics in a generation.

The End of the Interchange Tax

The most powerful argument for the merger is deceptively simple: today, no single railroad crosses the country. A container arriving in Los Angeles bound for Atlanta must be handed off — typically in Chicago, St. Louis, Memphis, or New Orleans — from a western carrier to an eastern one. That interchange is where freight goes to wait. Cars sit in yards for a day or more; crews change; paperwork changes; accountability changes. Shippers have long called it the “interchange tax,” and it is paid in time, money, and reliability.

A single-line transcontinental railroad eliminates that tax on thousands of lanes. One dispatching system, one operating plan, and one accountable carrier means a container can roll from the Port of Long Beach to the Port of Savannah without ever leaving the network. Union Pacific has argued that removing interchange delays could shave a full day or more off many coast-to-coast transit times. In a logistics economy where inventory carrying costs and delivery predictability drive purchasing decisions, that is a transformational improvement — and it changes the fundamental economics of choosing rail.

Taking On the Truck — and Winning

Here is the real competitive story: the merged railroad’s biggest rival isn’t another railroad. It’s the roughly 11 million heavy trucks moving freight on American highways. Rail has always been cheaper per ton-mile — a single intermodal train can carry the load of 250 to 300 trucks while moving a ton of freight hundreds of miles on a single gallon of fuel. What rail has historically lacked is the speed and door-to-door reliability that trucking offers.

Single-line transcontinental service closes that gap. When rail can match truck-competitive transit times on long-haul lanes at a fraction of the cost, shippers will convert — and every trainload converted means hundreds of semi trucks off the interstate. The public benefits compound: less highway congestion, less wear on taxpayer-funded roads, dramatically lower emissions per ton of freight, and fewer heavy trucks sharing the road with family cars. Large trucks are involved in thousands of fatal crashes each year; shifting long-haul volume to rail, which moves freight on a dedicated and separated right-of-way, is one of the most direct safety improvements available in American transportation.

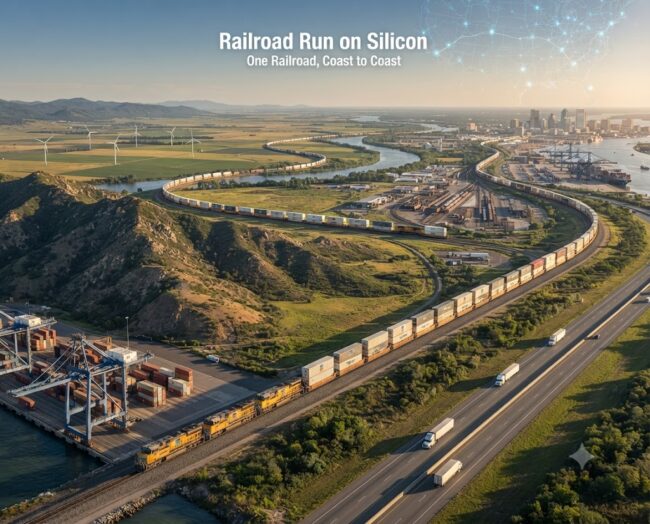

A Railroad Run on Silicon

The merger also arrives at the moment technology is remaking what a railroad can be. Modern Class I railroads are no longer just steel and diesel — they are rolling sensor networks. Machine-vision portals photograph every passing railcar at track speed and use AI to flag defects a human inspector might miss. Predictive maintenance models analyze data from trackside detectors to identify a failing wheel bearing weeks before it becomes a derailment risk — a capability with obvious resonance given the industry’s renewed focus on hazardous-materials safety.

Artificial intelligence is transforming operations, too. AI-assisted dispatching and network planning can optimize train meets, crew assignments, and terminal sequencing across the entire system in ways impossible with two separate networks and two separate operating plans. Energy-management software already functions as a cruise control for locomotives, cutting fuel burn on every run. A unified transcontinental network multiplies the value of all of these tools: one data platform, one AI-optimized operating plan, one end-to-end view of every shipment. For customers, that means Amazon-grade shipment visibility — real-time tracking and reliable delivery windows — applied to 10,000-ton trains.

The current logistics landscape for major carriers like Amazon, FedEx, and UPS relies on a mix of air, truck, and rail, with each company prioritizing different modes based on their service level agreements and operational models. The proposed merger between Union Pacific (UP) and Norfolk Southern (NS) into a “transcontinental” railroad would significantly alter the competitive math for these companies.

Current Use of Rail Service

- UPS: UPS has historically been the most significant user of rail among the three. They utilize intermodal rail (placing trailers on flatcars) for a large portion of their ground parcel traffic to move heavy loads over long distances more cost-effectively than trucking.

- FedEx: FedEx operates with a more segmented approach. Their “Express” (overnight) business relies heavily on air transport. Their “Ground” and “Freight” divisions primarily use trucking, partly because their network is built on a model of independent contractors and regional hubs that favor the flexibility of road transport over the slower, fixed schedules of rail.

- Amazon: Amazon has built a massive, “do-it-yourself” logistics network. They utilize a multimodal approach—trucks, aircraft, and containers—to manage their own supply chain. They are increasingly moving away from total reliance on third-party carriers, using their own trailers and hub-and-spoke centers to control every step of the journey, including rail for long-haul intermodal moves where it fits their cost-and-speed profile.

How the Merger Could Change the Calculus

The core promise of the UP-NS merger is the elimination of the “interchange tax”—the delay and complexity that occur when freight is handed off between two different railroads (typically in hubs like Chicago or Memphis).

1. Shift from Truck to Rail

The merger’s main competitive goal is to make rail more “truck-like.” Currently, long-haul trucking (over 800–1,000 miles) is the default for time-sensitive goods because rail handoffs add 24–48 hours of unpredictable “dwell time.”

The Change: A single-line, coast-to-coast network would remove these handoffs. If the merged railroad can guarantee reliable, faster transit times, Amazon, FedEx, and UPS may shift significant volumes of long-haul freight from over-the-road semi-trucks to rail. This is particularly attractive for non-urgent “Ground” shipments where cost efficiency is paramount.

Simplified Operations and Digital Integration

Currently, shipping across the country often requires two contracts, two invoices, and two different tracking systems.

- The Change: The merger promises a unified digital interface—one contract, one point of contact, and one real-time tracking dashboard. For logistics giants like Amazon, which prize end-to-end visibility and data-driven supply chain management, this simplification could reduce administrative overhead and improve their ability to plan and execute complex, cross-country logistics.

Increased Leverage and Pricing Power

- The Change: While the merger could provide cost savings and efficiency, there is a risk of reduced competition. Today, a shipper can often choose between different rail combinations (e.g., UP + CSX vs. UP + NS). A single-line “super-carrier” could theoretically exercise more pricing power. FedEx, UPS, and Amazon would need to balance the benefits of single-line efficiency against the potential for higher rates and a lack of alternative rail options on certain key lanes.

Strategic Reshoring

The merger could support a broader trend of companies moving manufacturing back to North America (nearshoring) by providing a reliable “land bridge” from Mexico or various U.S. ports to inland distribution centers. For Amazon and other retailers, this could mean faster access to stock for their regional fulfillment centers, further reducing the need for costly air-freight or long-haul truck “teams” to move goods from coastal ports.

Summary of Impact

For these companies, the merger effectively shifts the “competitive line” between truck and rail. By potentially shaving days off transit times and offering a single, accountable partner, the new rail network could turn rail from a “cheap but slow” option into a “cheap and reliable” backbone for national logistics, potentially putting millions of long-haul truckloads on the rails. However, the outcome heavily depends on whether the merged entity can actually deliver on its efficiency promises or if integration challenges cause the kind of service meltdowns seen in past rail mergers.

New Services a Split Network Could Never Offer

The most exciting possibilities are the services that simply cannot exist today. Think scheduled, truck-competitive transcontinental intermodal “land bridges” linking Pacific ports to Southeastern population centers in guaranteed transit times. Premium expedited lanes for parcel and e-commerce traffic. Single-carrier service for Mexican automotive plants shipping directly to East Coast distribution hubs, leveraging Union Pacific’s unmatched border gateways. New single-line routes for grain, chemicals, and energy products that today require costly, slow interchanges. Even domestic supply chains being reshored from overseas would find a coast-to-coast railroad a powerful enabler, connecting new Sun Belt factories to both coasts’ ports and markets.

The railroads have also pledged that the combination will be growth-oriented rather than a cost-cutting exercise — keeping gateways open, honoring existing interchange agreements, and competing for freight that currently never touches a train. If the merged company delivers on that vision, the winners are not just shareholders but every American who buys goods that move — which is to say, everyone.

The Bottom Line

The first transcontinental railroad, completed in 1869, bound a young nation together. A century and a half later, its corporate descendant proposes to finish the job: a single, AI-powered, coast-to-coast freight network that is faster than the fragmented system it replaces, cheaper than the highway, and safer than the truck. That is a rare merger whose benefits extend well beyond the boardroom — onto the highways it decongests, into the supply chains it accelerates, and across the economy it helps move.

A note on the other side of the ledger: the merger remains under Surface Transportation Board review, and it has serious critics. Shipper groups, some labor unions, and competition advocates warn that consolidating an industry already dominated by a handful of carriers could reduce competition, raise rates for captive shippers, and repeat the service meltdowns that followed past rail mergers. Rivals such as BNSF and CSX have raised concerns about network access, and regulators must weigh whether promised benefits will materialize or whether conditions — like guaranteed open gateways and reciprocal switching — are needed to protect customers. Any full assessment of the deal should take those arguments seriously.

About Brian French

Led by a commitment to tech-intelligent curation, Brian French tracks and analyzes the corporate developments defining Florida's economy. Brian brings an extensive financial background to his analysis, having graduated from the University of South Florida in Finance and serving as a Vice President and Portfolio Manager for Merrill Lynch Private Investors and the Trust Department in St. Petersburg, FL, as well as a Vice President and Trust Investment Officer for SunTrust Bank in Sarasota, FL. His writing blends macroeconomic trends, fiduciary capital markets, corporate strategy, and modern digital insights for a sophisticated look at Florida's business market.